Material Vs. Immaterial Change Processing Options in Oracle Revenue Management Cloud Services

Introduction:

Oracle Revenue Management Cloud Services has two options to process changes Contract after contract Freeze date on Revenue Contract.

- Material Changes

- Immaterial Changes

Changes could be on any of the below given source data:

- Unit Sell Price (It can only allow on Material Change)

- Extended Sale Price

- Quantity

- Revenue Start date

- Revenue End date

- Contract Termination Date

- Adding New Line or New POB (Performance Obligation)

What is the Challenge to select the correct option?

As an Implementer, I see a huge challenge identifying an appropriate option to modify the Revenue contract in RMCS.

A typical example of a common challenge:

The Business user says he has a “Material Rights addition or Change on Revenue Contract.” Still, when you see the use case, you understand that it can only be achieved by the “Immaterial Option available in RMCS,” not by the Material change option. It is very critical to decide the right processing options upfront.

What is the difference between both options in RMCS?

Material Change options possess the below rules:

- Identify New / Changed data

- Reverse Revenue from All Lines

- Re-Allocate All Lines (New + Existing)

- Re-Recognize Revenue using New Allocation Prices

- Accounting is Retrospective for Revenue Events already happened

Material Change options possess the below rules:

- Identify New / Changed data

- Reverse Recognized Revenue after Contact Revision Date only for Open Obligation Line/s and recognized after the revision date

- Derive Unrecognized Revenue

- Re-allocate only New line/Changed Lines and Open Obligation line

- New Event Will Recognize Revenue after Contract Revision Date

- Accounting is Prospective (Revenue Intact, which is already Recognized)

Example:

Material Changes

Original Contract:

Transaction Price: 1257

Rev Rec: 1153.63 (Till date)

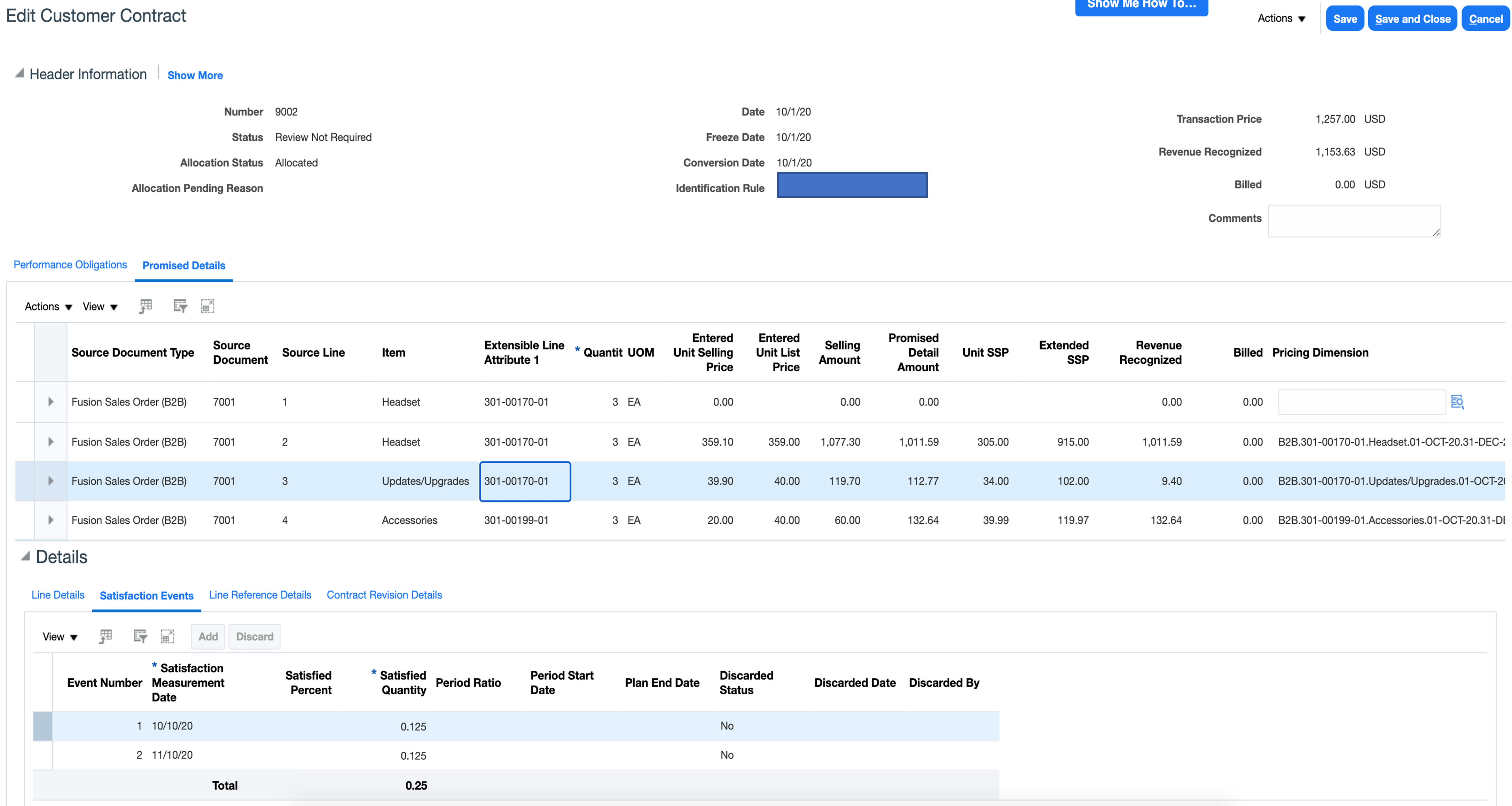

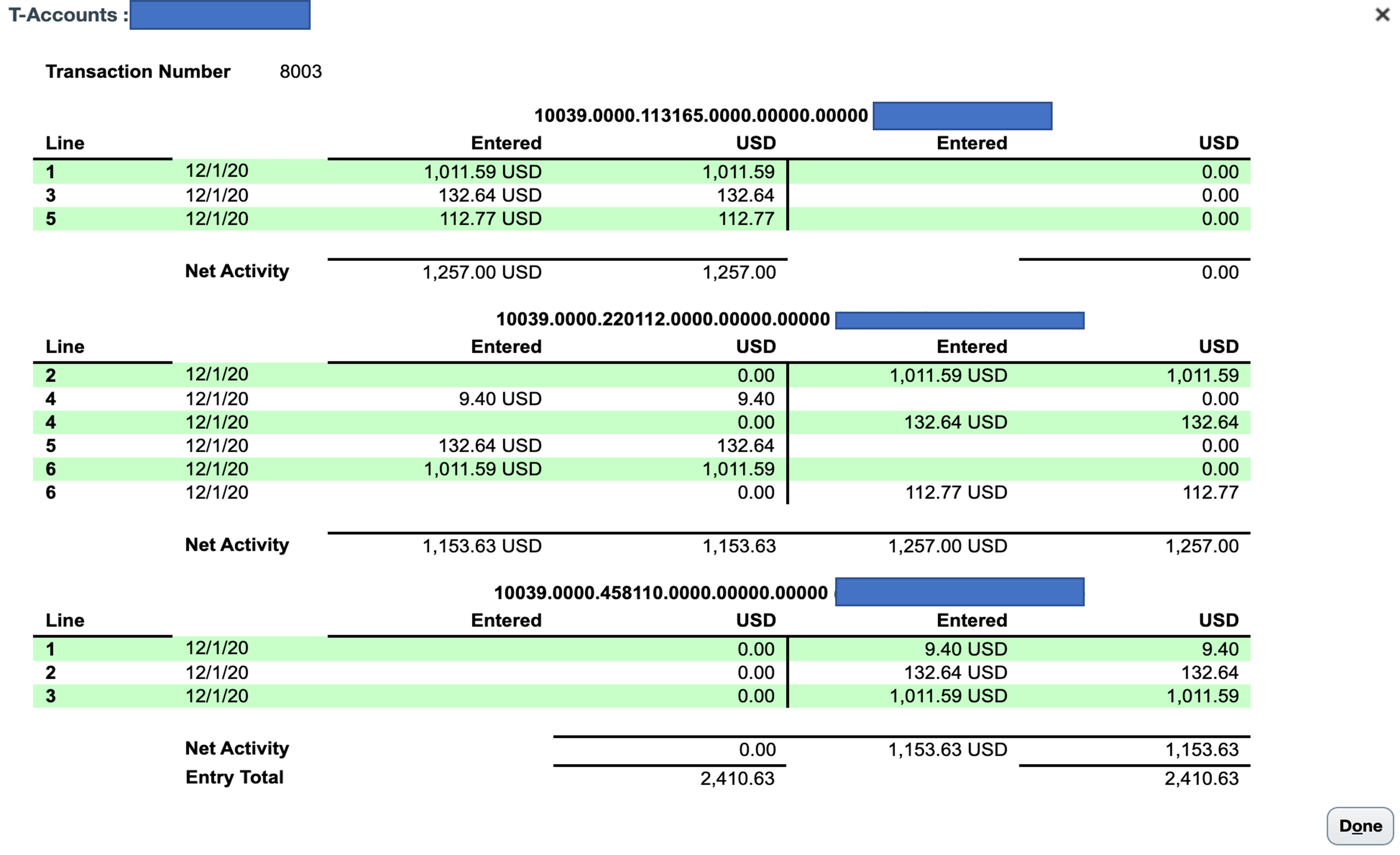

Original Contract Activities before Material Changes

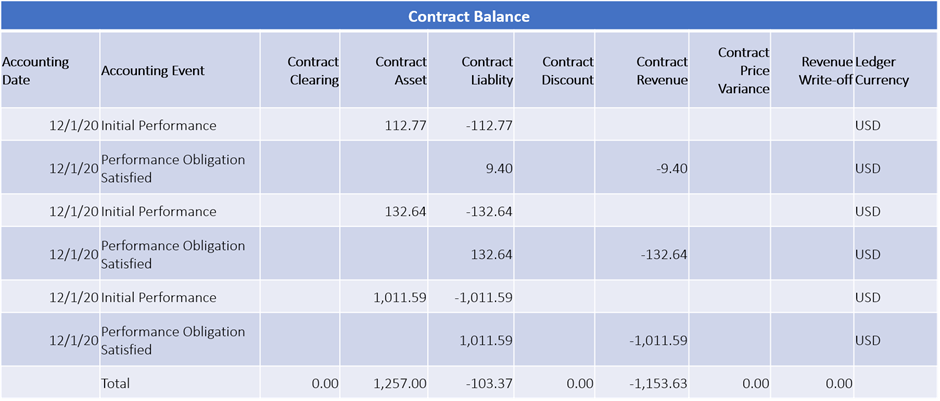

Original Contract Activities before Material Changes Original Contract Accounting before Material Changes

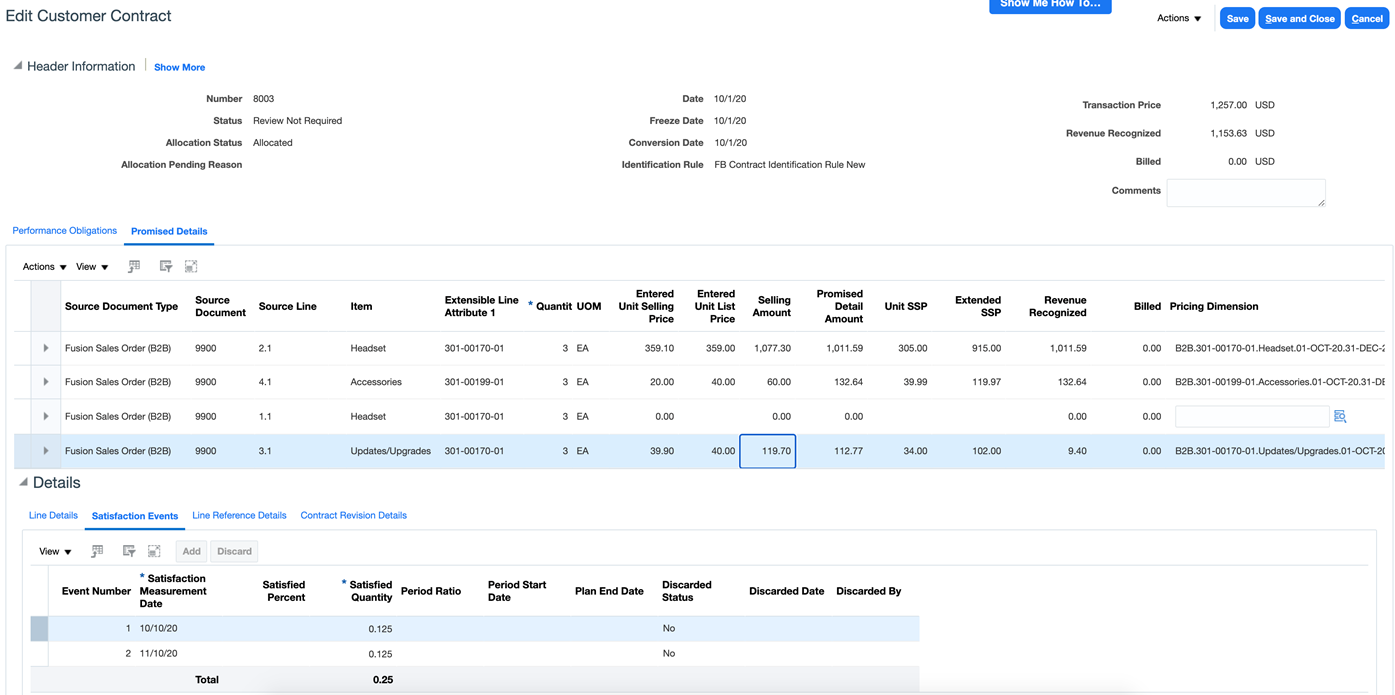

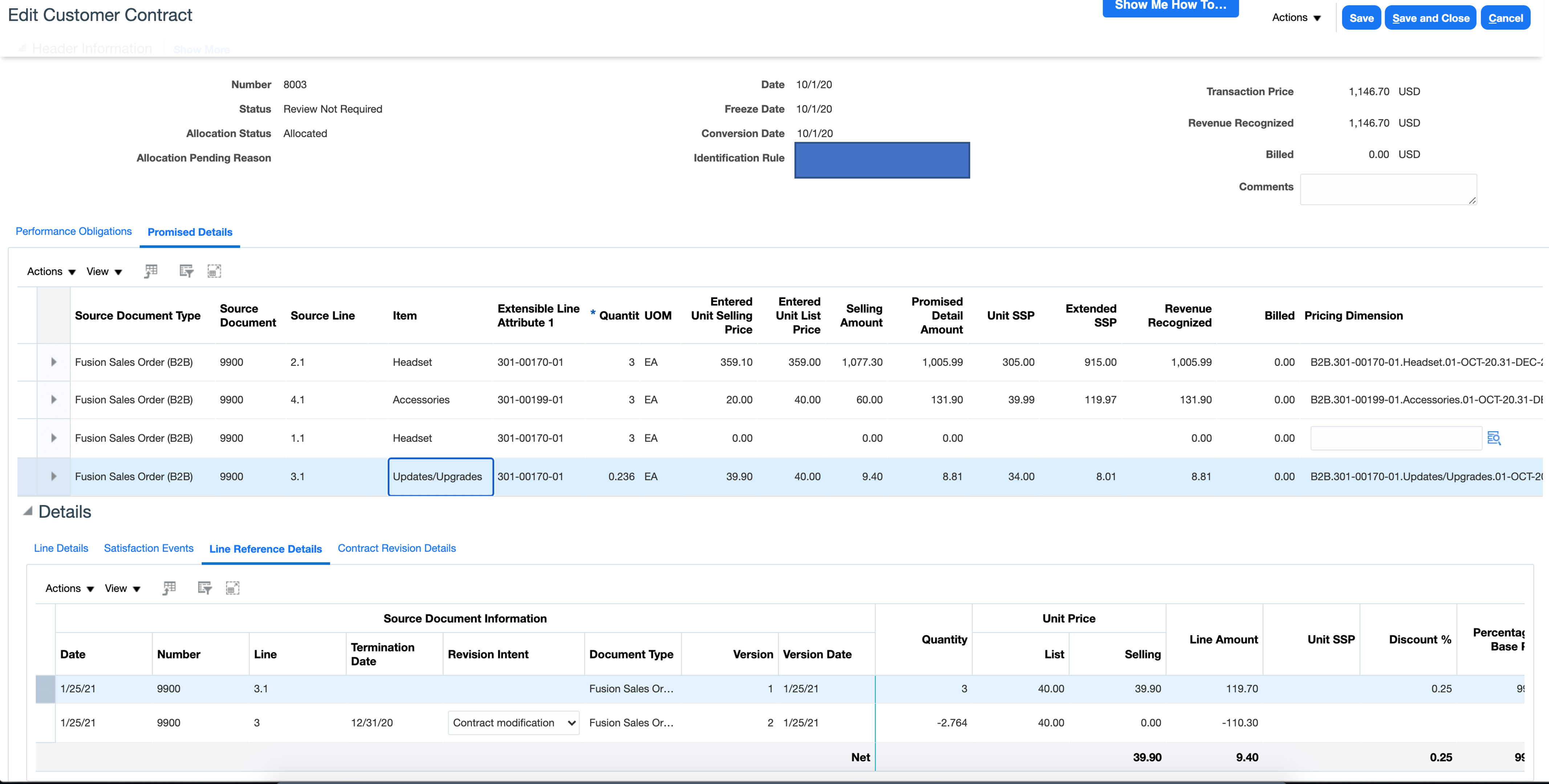

Original Contract Accounting before Material Changes We have change on Line 3 where Qty and Unit Price is changed

We have change on Line 3 where Qty and Unit Price is changed

- Old Line Unit Sell Amount = 39.90, New Line Unit Sell Amount = 9.40

- Old Line Qty = 3, New Line Qty = 1

- Original Contract: Transaction Price: 1257, Rev Rec: 1153.63 Till date

- Modified Contract: Transaction Price: 1146.70, Rev Rec: 1119.35 Till date

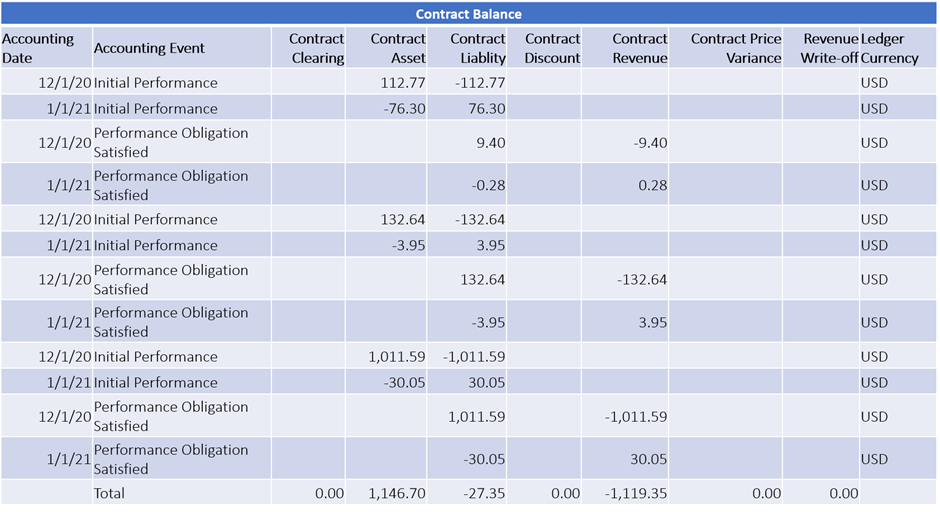

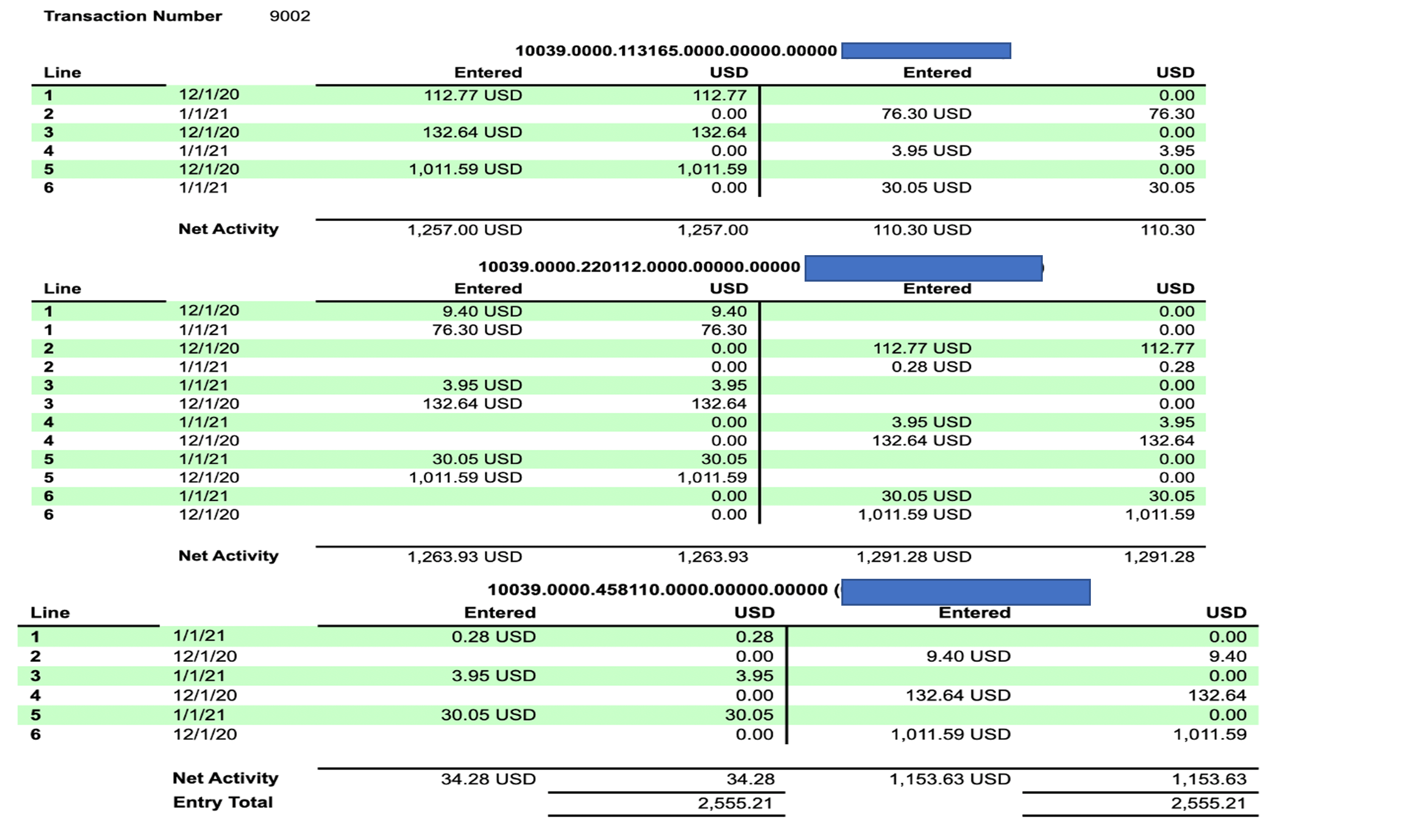

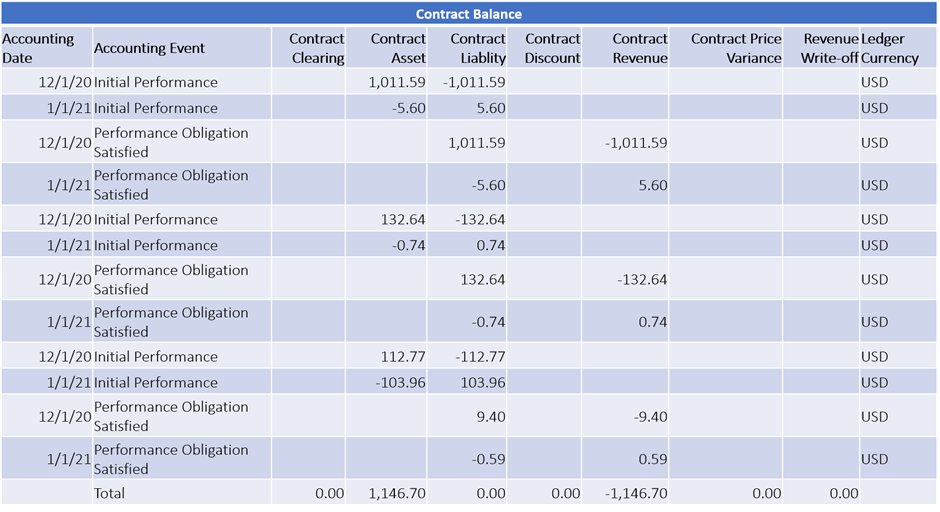

Activities After Material Changes

Activities After Material Changes

- Revenue Activities Reversed

- Re-allocation Performed

- Revenue Catch Up in Current Period

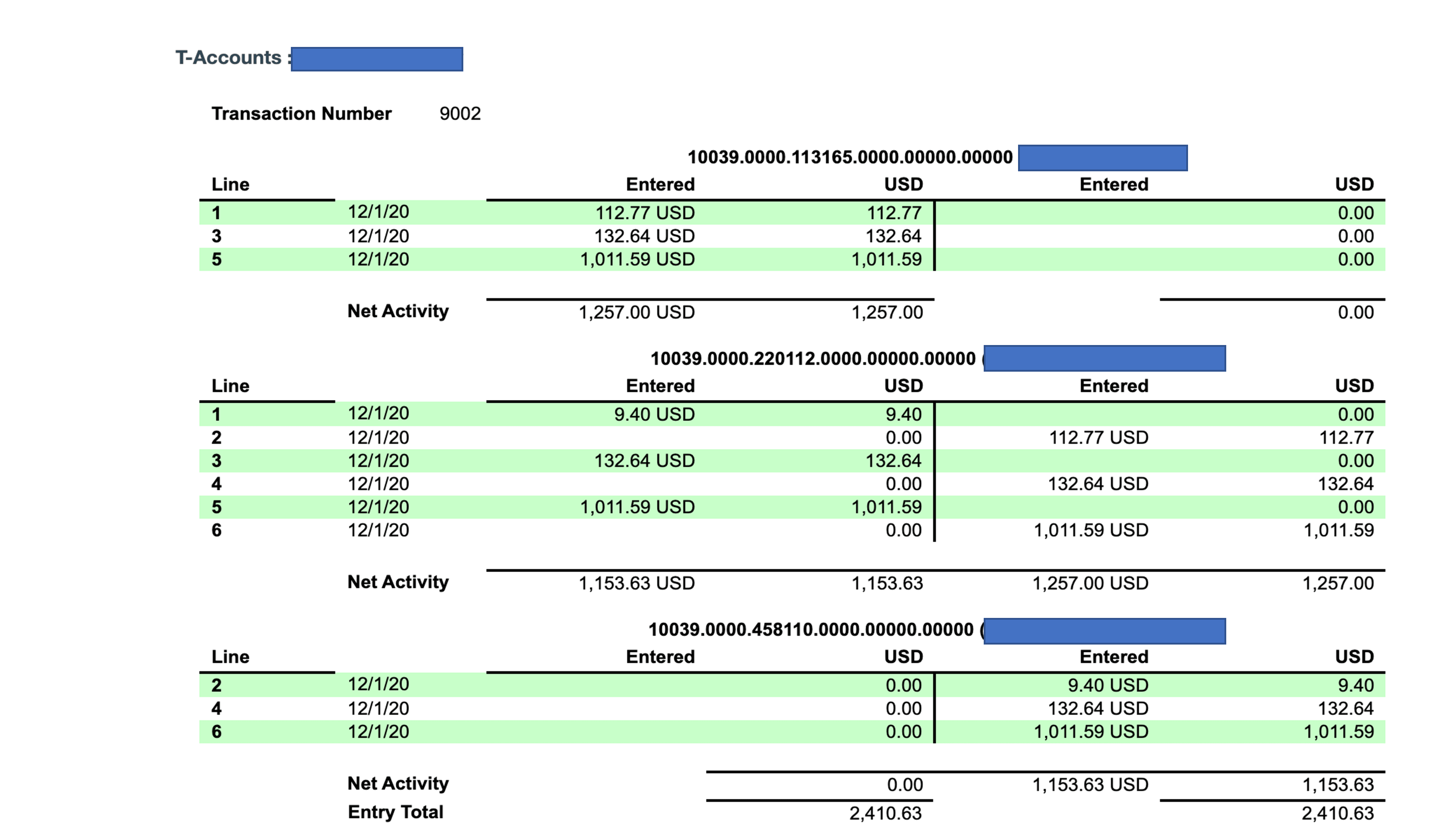

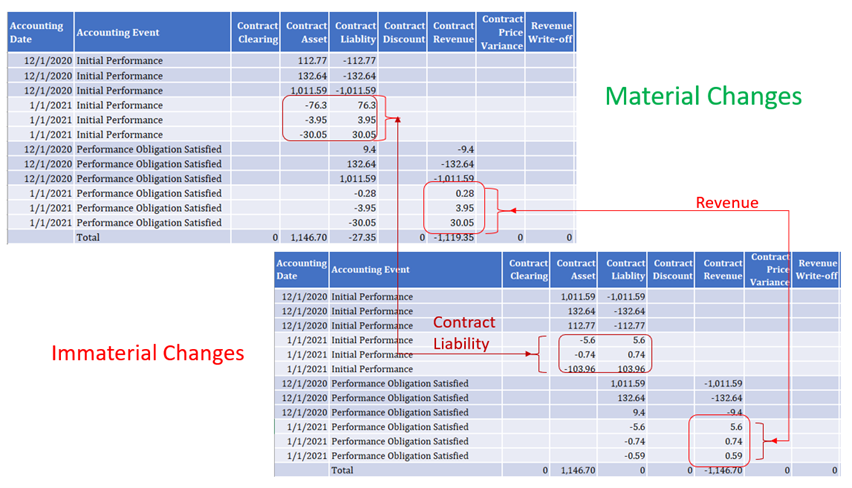

Accounting after Material Changes

Accounting after Material Changes

- Revenue Accounting Reversed

- Re-allocation Performed

- Revenue Catch Up Accounting in Current Period

Immaterial Changes

Immaterial Changes

Original Contract:

Transaction Price: 1257

Rev Rec: 1153.63 (Till date)

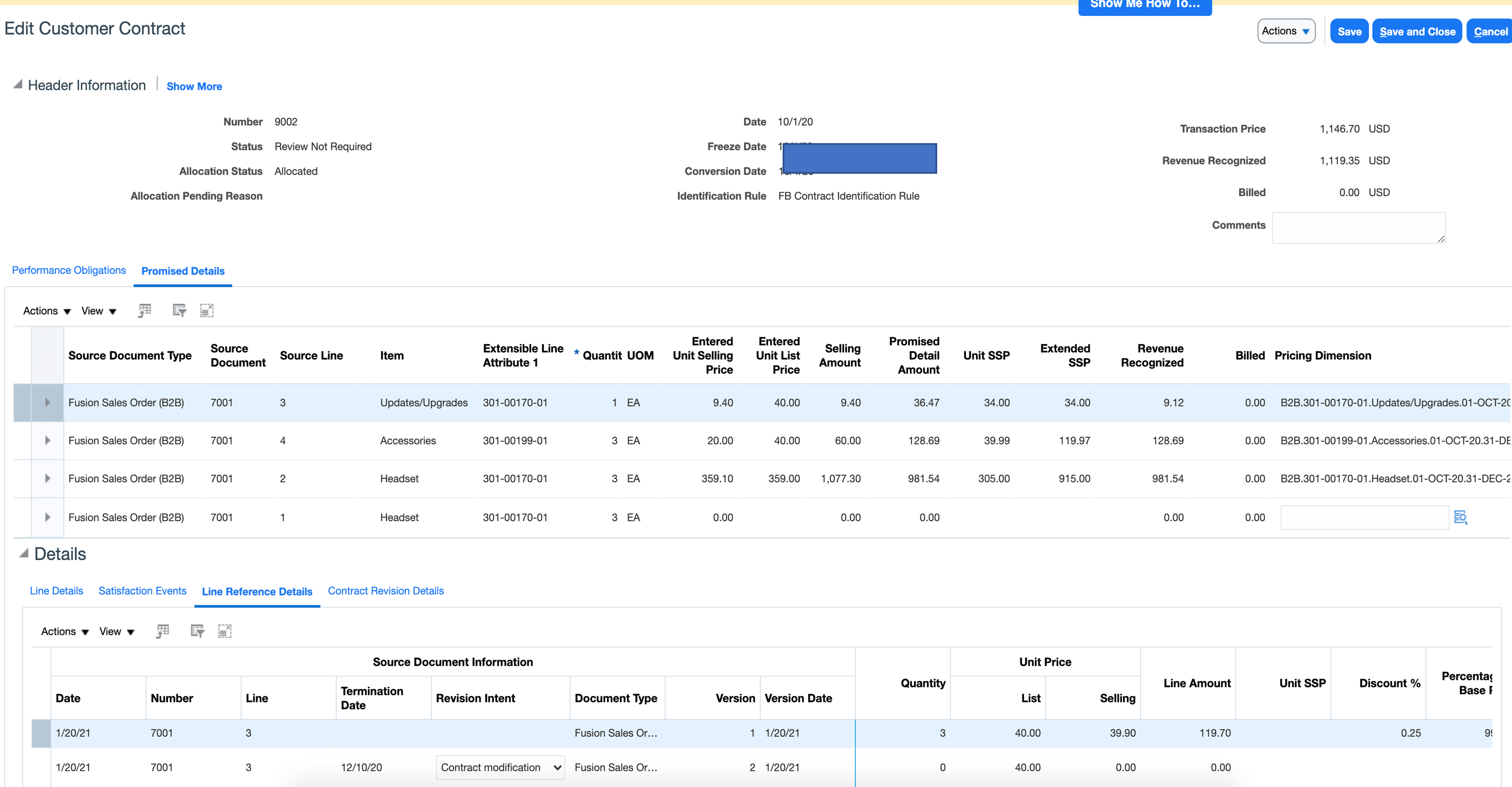

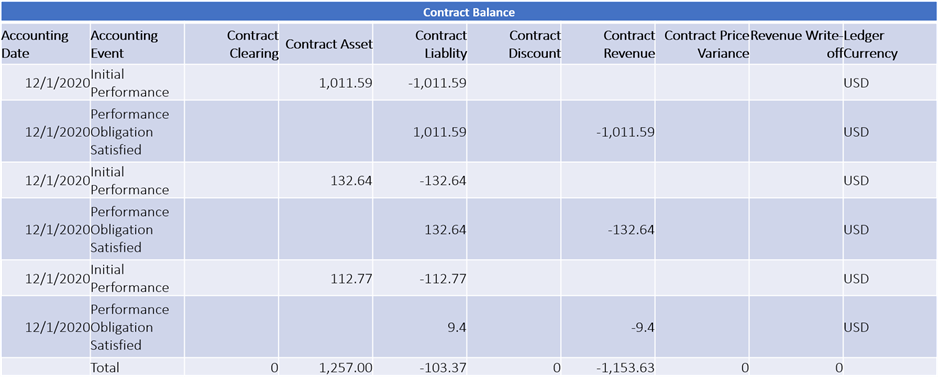

Original Contract Activities before Immaterial Changes

Original Contract Activities before Immaterial Changes Original Contract Accounting before Immaterial Changes

Original Contract Accounting before Immaterial Changes We have change on Line 3 where Qty and Extended Unit Price is changed

We have change on Line 3 where Qty and Extended Unit Price is changed

- Old Line Extended Sell Amount = 39.90 New Line Extended Sell Amount = 9.40

- Old Line Qty = 0.236 New Line Qty = 1

- Original Contract : Transaction Price: 1257 , Rev Rec: 1153.63 Till date

- Modified Contract: Transaction Price: 1146.70, Rev Rec: 1146.70 Till date

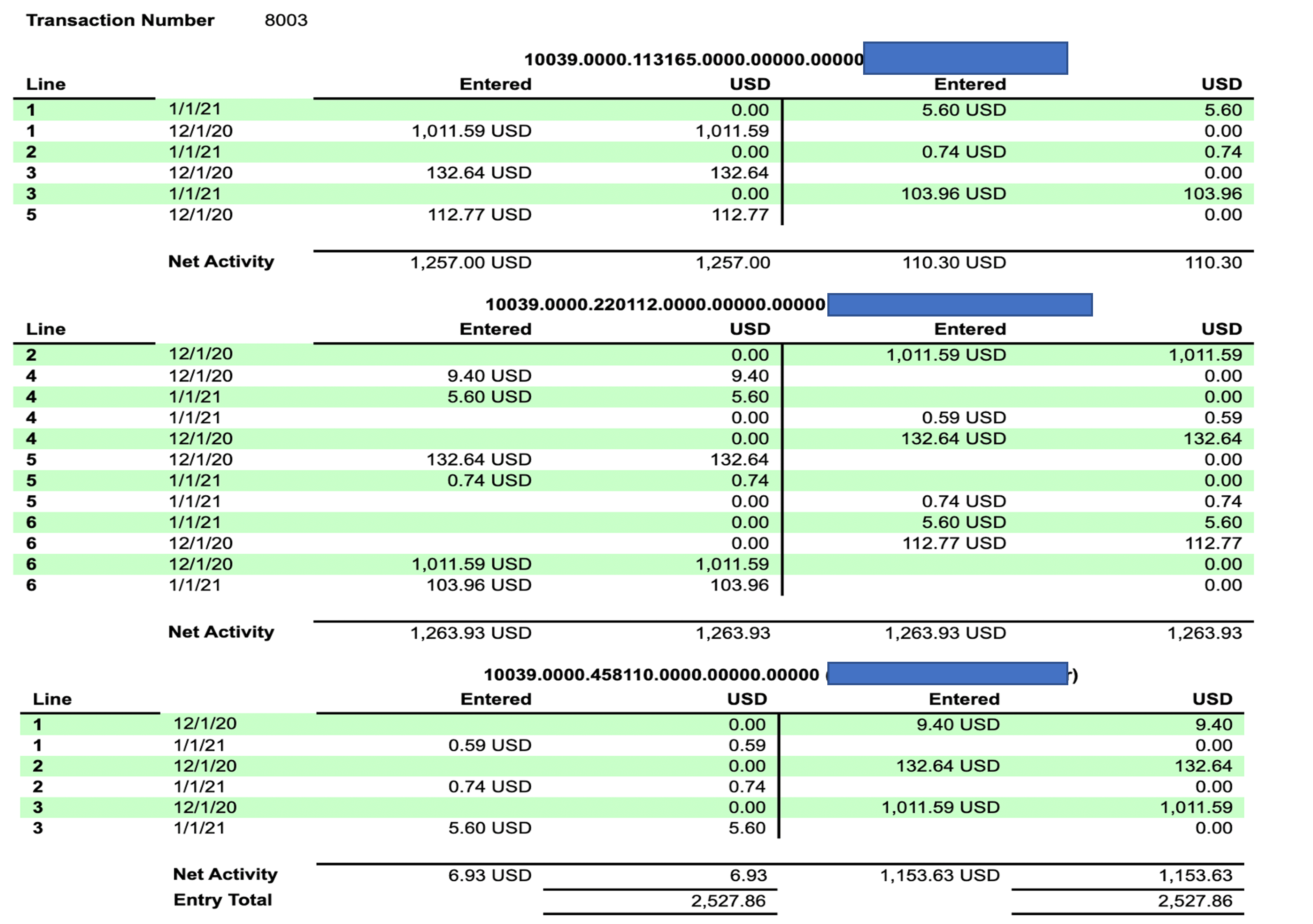

Activities After Immaterial Changes

Activities After Immaterial Changes

- Revenue Activities Reversed only from future dates and Open Obligation Lines

- Re-allocation Performed between Open lines

- Revenue in Current Period

Accounting after Immaterial Changes

Accounting after Immaterial Changes

- Revenue Activities Reversed only from future dates and Open Obligation Lines

- Re-allocation Performed between Open lines

- Revenue in Current Period

Conclusion:

It is clear from the above example that the Revenue contract modification option has 2 fundamental differences in terms of Recognize Revenue and Allocation.

Material change option always works on Retrospective accounting while Immaterial change Option works on Prospective accosting approach.

Besides this, we should also note that you will not change the Unit Sell price using the Immaterial option; while utilizing the Material option, you can adjust all 3 Quantity, Unit Sell, and Extended Sell price.

Comments

Post a Comment